Long-term liabilities, which are also known as noncurrent liabilities, are obligations that are not due within one year of the balance sheet date.

Three examples of long-term liabilities include:

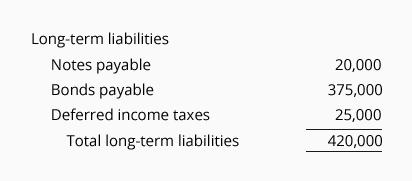

Here is the long-term liability section from our sample balance sheets:

When notes payable appears as a long-term liability, it is reporting the amount of loan principal that will not be payable within one year of the balance sheet date.

To illustrate, assume that a company signed a promissory note on December 31, 2023 for a loan of $120,000. The loan requires the interest to be paid at the end of every month. The loan’s principal of $120,000 is required to be paid as follows:

The company’s December 31, 2023 balance sheet will report the $120,000 of principal owed as follows:

The company’s December 31, 2024 balance sheet will report the remaining $80,000 of principal owed as follows:

Another example of a long-term liability is a mortgage loan for a company’s office building. (A mortgage loan is a loan secured by a lien on real estate.) Assuming the mortgage loan requires monthly payments of interest and principal, the total of the 12 loan principal payments following the date of the balance sheet will be reported as the current liability current portion of long-term debt. The principal balance remaining after those 12 principal payments is reported as the long-term liability mortgage loan payable. (For an example of this calculation, see our Business Form G-7 Current Portion of Long-term Debt.)

Bonds payable are long-term debt securities issued by a corporation. Typically, bonds require the issuer to pay interest semi-annually (every six months) and the principal amount is to be repaid on the date that the bonds mature. It is common for bonds to mature (come due) 10-20 years after the bonds were issued.

A corporation that issues bonds will often have some balance sheet general ledger accounts associated with the bonds (Bonds Payable, Bond Issue Costs, Discount on Bonds Payable, Premium on Bonds). The balances in these accounts are likely combined into a single amount.

Any bond interest that has accrued but has not been paid as of the balance sheet date is reported as the current liability other accrued liabilities.

You can learn about bonds by visiting our topic Bonds Payable.

Often the amount reported as the long-term liability deferred income taxes pertains to the difference between the amounts of depreciation expense reported on a regular U.S. corporation’s financial statements vs. the amounts of depreciation expense reported on the corporation’s income tax returns. The amount results from the timing of when the depreciation expense is reported.

Please let us know how we can improve this explanation

Submit Feedback No ThanksThe final liability appearing on a company’s balance sheet is commitments and contingencies along with a reference to the notes to the financial statements. No amount is shown on the balance sheet for this item.

The notes for commitments and contingencies could include the following disclosures:

Please let us know how we can improve this explanation

Submit Feedback No ThanksIf a business is organized as a corporation, the balance sheet section stockholders’ equity (or shareholders’ equity) is shown beneath the liabilities. The total amount of the stockholders’ equity section is the difference between the reported amount of assets and the reported amount of liabilities. Similar to liabilities, stockholders’ equity can be thought of as claims to (and sources of) the corporation’s assets.

(If the business is a sole proprietorship, this section appears as owner’s equity. We will discuss owner’s equity later.)

The stockholders’ equity section will report the following items as separate amounts:

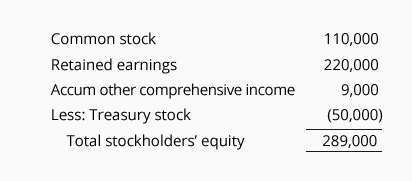

Here is the stockholders’ equity section from our sample balance sheets:

Common stock reports the amount a corporation received when the shares of its common stock were first issued.

NOTE: Some of the states in the U.S. require that a corporation’s shares of common stock have a par value. If so, the amount the corporation received when the shares were issued is divided between two lines that are reported within the stockholders’ equity section:

A relatively small percent of corporations will issue preferred stock in addition to their common stock. The amount received from issuing these shares will be reported separately in the stockholders’ equity section.

The amount the corporation received from issuing shares of stock is referred to as paid-in capital and as permanent capital.

For many successful corporations, the largest amount in the stockholders’ equity section of the balance sheet is retained earnings. Retained earnings is the cumulative amount of 1) its earnings minus 2) the dividends it declared from the time the corporation was formed until the balance sheet date.

It is important to realize that the amount of retained earnings will not be in the corporation’s bank accounts. The reason is that corporations will likely use the cash generated from its earnings to purchase productive assets, reduce debt, purchase shares of its common stock from existing stockholders, etc.

The stockholders’ equity section may include an amount described as accumulated other comprehensive income. This amount is the cumulative total of the amounts that had been reported over the years as other comprehensive income (or loss).

Three examples of other comprehensive income (or loss) that resulted in the amount reported in the stockholders’ equity section as accumulated other comprehensive income are:

Treasury stock is a subtraction within stockholders’ equity for the amount the corporation spent to purchase its own shares of stock (and the shares have not been retired).

When the corporation purchases shares of its stock, the corporation’s cash declines, and the amount of stockholders’ equity declines by the same amount. Hence, the cumulative cost of the treasury stock appears in parentheses.

NOTE: One of the financial statements issued by a corporation is the statement of stockholders’ equity. This financial statement summarizes the changes in the components of stockholders’ equity for each of the most recent three years.

To learn more about the components of stockholders’ equity, visit our topic Stockholders’ Equity.

Please let us know how we can improve this explanation

Submit Feedback No ThanksSince our sample balance sheets focused on the stockholders’ equity section of a corporation, we want to discuss the comparable section for a business organized as a sole proprietorship.

The balance sheet of a sole proprietorship will report owner’s equity instead of a corporation’s stockholders’ equity. Hence, a sole proprietorship’s balance sheet will resemble the accounting equation: assets = liabilities + owner’s equity.

The owner’s equity section of a sole proprietorship owned by J. Ott will have two general ledger accounts in which amounts are recorded:

The account J. Ott, Capital is the main owner’s equity account. Its balance is carried forward to the following year.

The account J. Ott, Drawing is used to record the owner’s withdrawals of cash (or other assets) during the accounting year. The owner’s draws are not reported as an expense on the company’s income statement, but they do cause a decrease in the owner’s capital. (At the end of the accounting year, a closing entry transfers the debit balance in J. Ott, Drawing to the account J. Ott, Capital.)

Typically, the change in the amount of owner’s equity for a sole proprietorship business is the result of:

The combination of the last two bullet points is the amount of the company’s net income.

Please let us know how we can improve this explanation

Submit Feedback No ThanksUsually a claim on an asset that is pledged as collateral. The lien is usually filed with a

government office.

Generally a long term liability account containing the face amount, par amount, or maturity amount of the bonds issued by a company that are outstanding as of the balance sheet date.

To learn more about bonds payable, see our Bonds Payable Outline.

Bond Issue Costs is a contra liability accounts reported along with Bonds Payable. Bond Issue Costs include the professional fees and registration fees associated with the issuance of bonds. The amount in the account Bond Issue Costs will be amortized (systematically written off) to interest expense over the life of the bonds.

A contra liability account that reports the amount of unamortized discount associated with bonds that are outstanding. The discount on bonds payable originates when bonds are issued for less than the bond’s face or maturity amount. The debit balance in this account will be amortized to bond interest expense over the life of the bonds and results in more interest expense than interest paid. To learn more, see Explanation of Bonds Payable.

A liability account with a credit balance associated with bonds payable that were issued at more than the face value or maturity value of the bonds. The premium on bonds payable is amortized to interest expense over the life of the bonds and results in a reduction of interest expense. To learn more, see Explanation of Bonds Payable.

The income statement account which contains a portion of the cost of plant and equipment that is being matched to the time interval shown in the heading of the income statement. (There is no depreciation expense for land.)

Also referred to as footnotes. These provide additional information pertaining to a company’s operations and financial position and are considered to be an integral part of the financial statements. The notes are required by the full disclosure principle.

A simple form of business where there is one owner. Legally the owner and the sole proprietorship are the same. However, for accounting purposes the economic entity assumption results in the sole proprietorship’s business transactions being accounted for separately from the owner’s personal transactions.

A class of corporation stock that provides for preferential treatment over the holders of common stock in the case of liquidation and dividends. For example, the preferred stockholders will be paid dividends before the common stockholders receive dividends. In exchange for the preferential treatment of dividends, preferred shareholders usually will not share in the corporation’s increasing earnings and instead receive only their fixed dividend.

A distribution of part of a corporation’s past profits to its stockholders. A dividend is not an expense on the corporation’s income statement.

A corporation’s own stock that has been repurchased from stockholders. Also a stockholders’ equity account that usually reports the cost of the stock that has been repurchased.